Dow Jones, DAX 40, Nikkei 225, Monthly Seasonality – Educational Report:

- Seasonality is when we observe regular patterns at fixed intervals in a year

- We can identify statistically meaningful seasonality for global stock markets

- While there are good and bad months, seasonality is a very poor predictor

Have you ever wondered whether or not certain months of the year are consistently better or worse for stock markets? If such a relationship does exist, then we would describe it as seasonal. Seasonality is something you often see in all kinds of data. For example, you can probably guess which months of the year ice cream sales consistently spike or when people repeatedly purchase more winter clothing.

Businesses use seasonality every year to plan their ventures, but can investors do the same with stock markets? If we assume that markets are efficient, reflecting all available information at a given time, then changes in stock prices every day (or in this case every month) should behave as white noise. In other words, we should not be able to predict the future based on past performance because markets are random.

I will put this simplified theory to the test for global stock markets. We will analyze the Dow Jones, S&P 500 and Nasdaq Composite on Wall Street. Then, we will do the same for the DAX 40, FTSE 100 and CAC 40 to gauge European indices. Finally, I will wrap up with a few major benchmark indices from the Asia-Pacific region: the Nikkei 225, ASX 200 and Hang Seng Index.

Each heatmap chart below contains identical parameters:

- Average monthly percent change (+2.5 means the index rose 2.5% on average in that month)

- Which months are significant (based on a 95% confidence interval from a regression model)

- The average goodness of fit between the 3 regression models (1 for each stock index)

These parameters will be discussed in further detail below.

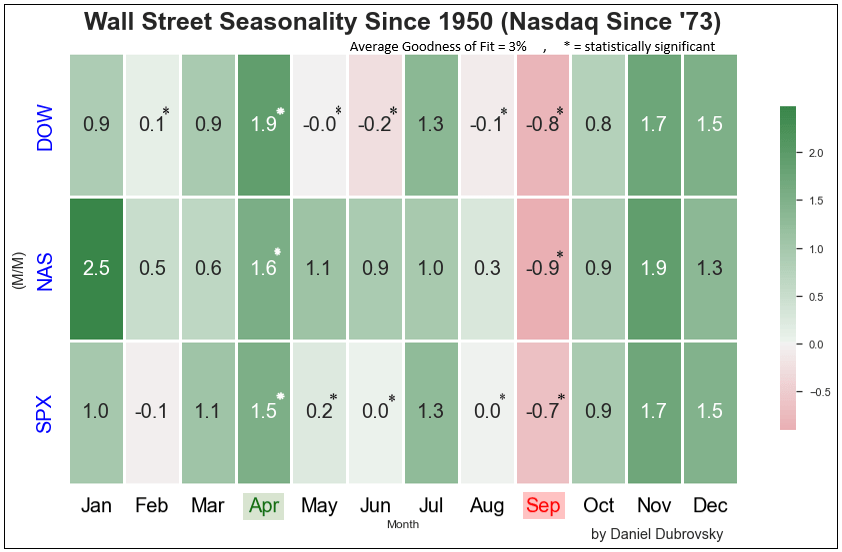

Dow Jones, S&P 500, Nasdaq Composite Monthly Seasonality

Starting with Wall Street, I have used data on the Dow Jones and S&P 500 since 1950. For the Nasdaq Composite, information since 1973 was used. The most recent month pulled was from December 2022, which applies to all European and Asia-Pacific indices as well. Are there any seasonal effects? Yes!

Historically, it seems that April has been the best month for Wall Street. On average the Dow, S&P and Nasdaq rallied +1.67% in this month. These are also statistically significant. In other words, there is about a 2.6% chance that this +1.67% effect on Wall Street is due to chance within the context of this study.

Meanwhile, September is the only month where all 3 indices have averaged negative and are statistically significant. In this month, the indices averaged -0.8%. I have also highlighted which other months are statistically significant with a “*”. Note that January seems to be a very strong month for the Nasdaq, but it is not significant because, over the years, this month has become progressively weaker.

Finally, and arguably more importantly, notice that the average goodness of fit between the 3 models is 3% (out of a maximum of 100%). What does that mean? On average, about 3% of the variation on Wall Street since the 1950s (‘70s for the Nasdaq) can be explained by seasonality alone (without factoring in any other variables like monetary policy or the unemployment rate).

In other words, while we found meaningful seasonality in April and September, seasonality by itself did a very poor job of explaining how stock markets traded in these months.

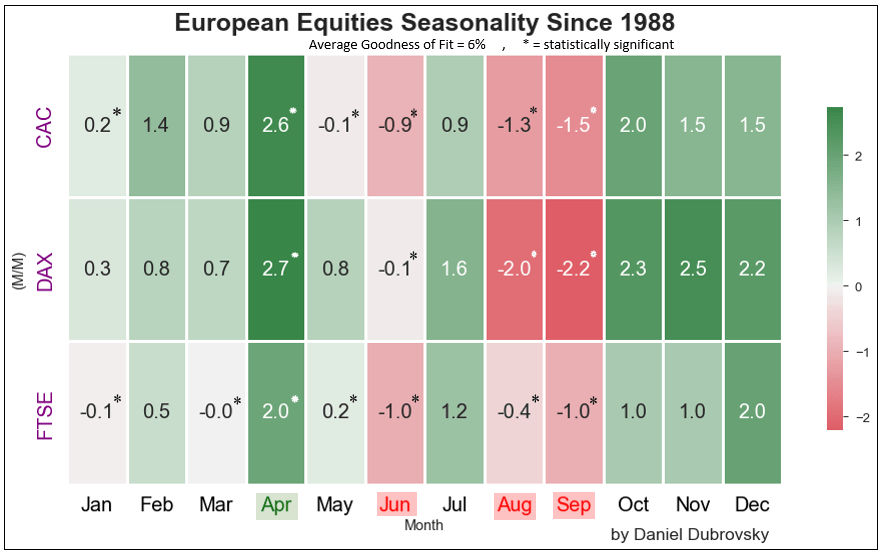

DAX 40, FTSE 100, CAC 40 Monthly Seasonality

Now let us switch to European indices. It should be noted that the data is not as comprehensive as Wall Street, only going back to 1988. This means that compared to the Dow Jones and S&P 500, we have almost half the number of observations for the DAX 40 (German), FTSE 100 (United Kingdom) and CAC 40 (France).

Still, April has consistently been the best month, similarly to Wall Street. In this month, these European indices averaged 2.43%. For all 3 of them, this month is statistically significant.

Meanwhile, June, August and September have consistently been some of the worst months, averaging -0.67%, -1.23% and -1.57%, respectively. These are all statistically significant. As such, it seems you can find more weak months for this corner of global stock exchanges.

Similarly, with Wall Street, the average goodness of fit for seasonality in European indices is quite low at 6%. Once again this means that while we can identify meaningful seasonality, by itself it is not a good indicator of how these markets have performed in April, June, August and September over the years.

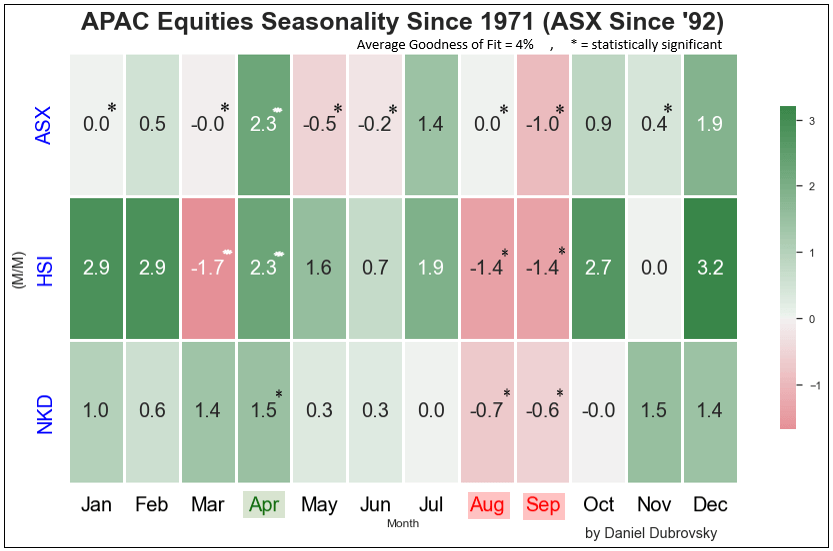

Nikkei 225, ASX 200, Hang Seng Index Monthly Seasonality

Wrapping up with Asia-Pacific markets, we will be analyzing the Nikkei 225 (Japan) and Hang Seng Index (Hong Kong) since 1971, along with the ASX 200 (Australia) since 1992.

Much like with Wall Street and European indices, April appears to have consistently and significantly been the best month for these APAC stock markets. The Nikkei 225, Hang Seng Index and ASX 200 averaged about 2% over the years.

Meanwhile, August and September have consistently and significantly been the worst periods. During these months, the indices returned -0.7% and -1% on average, respectively.

Like with other markets, the average goodness of fit was approximately 4%. Once again, while we can identify meaningful seasonality, by itself it did not do a good job of explaining how these markets performed in April, August and September over the years.

Should We Care About Seasonality in Stock Markets?

The takeaways from this deep dive can be split up into 4 key findings:

- Statistically significant seasonality is present in global stock markets

- April has consistently been the best month between the US, Europe and Asia

- September is the only month between all areas that has consistently disappointed

- Seasonality by itself has been a poor predictor of performance

For those with a keen eye, you might have noticed that October, November and December have historically been strong months for these global markets. But, as tested with the regression model, for the most part, these months have not been statistically significant.

With that in mind, while we can identify reoccurring patterns in global stock markets, which to a certain extent pours cold water on the “white noise” hypothesis, it probably will not hurt much to brush aside these effects in analyzing stock markets generally.

Trading Strategies and Risk Management

Global Macro

Recommended by Daniel Dubrovsky

--- Written by Daniel Dubrovsky, Senior Strategist for DailyFX.com